Property Crowdfunding – Equity v Debt Investments

Both debt and equity crowdfunded investment have become incredibly popular vehicles for the property investment since their genesis five years ago.

Both debt and equity crowdfunded investment have become incredibly popular vehicles for the property investment since their genesis five years ago.

Both equity and debt fundraising involve the raising of finance from a crowd of individuals, pooling their resources for a common project. This often means that both find themselves lumped under the umbrella term of ‘property crowdfunding’. Nonetheless, peer-to-peer lending and crowdfunding have some distinct differences.

Let me clarify some of those differences for you.

Let’s begin with a word about Diversification in investment.

The first rule of investing is to diversify, in order to spread your risk. As such, it usually makes more sense to spread your investments over both equity and debt-based (P2P) investments. This also allows you to benefit from the tax breaks afforded to both vehicles.

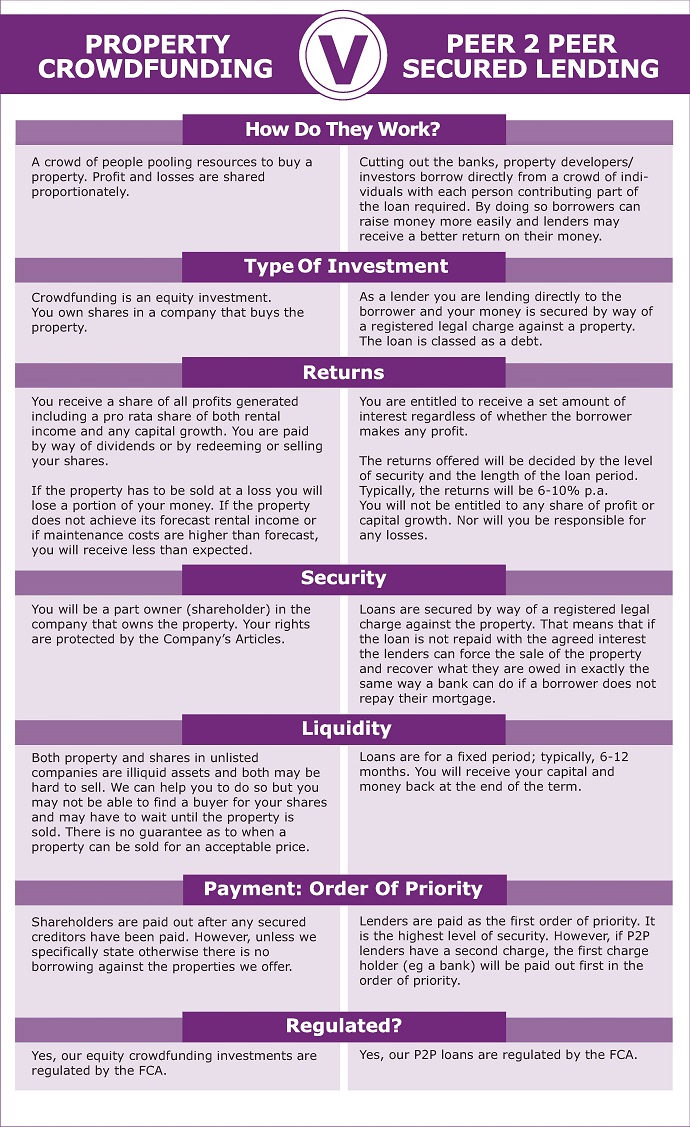

Before we get into a full explanation of Equity versus secured P2P lending, here’s a visual comparison of the two different structures:

Equity Crowdfunding

In exchange for your investment, with equity crowdfunding you will acquire shares in a company. You’ll also gain entitlement to a share of rent and sale income as a dividend. However, where no profit exists to be shared, you will not receive a dividend.

There’s the risk of losing money if the property purchased through the investment falls in value. This is because, along with that loss, your shares will also fall in value.

If you would like to sell your shares at any point, if you can find a buyer you are free to do so. You should bear in mind that any profit from the sale of your shares will likely be subject to capital gains tax, though. That is, of course, once your annual allowance has been taken into account.

Most people believe that ownership provides more security. However, it’s vital to understand that, when an asset, such as a house, is sold, any loans that are taken out against that property will be paid off before shareholders receive their dividend. As such, the creditors are in a stronger position in many ways than the actual shareholders and property owner.

Despite these potential downsides, equity crowdfunding is the preferred option for many. There’s that sense of some solid investment asset, a real share in property. Also, there’s the benefits of profit from both rental income and any capital growth.

Investment in property has long been proven one of the best ways to raise a healthy retirement income. Crowdfunding allows you to do this without all the hassle that, in the past, has been entailed in property investment. It’s not a quick win, though, and should be considered a medium to long term investment.

Another note, particularly for Muslim investors: equity investments like these, where risk and reward are shared, are usually considered Sharia compliant. Though, of course, this is down to your own personal beliefs.

Equity crowdfunding can also be a tax efficient investment. As from April 2016, the first £5,000 worth of dividend income received is tax-free.

Debt-Based Property Crowdfunding (aka Peer-to-Peer Secured Lending)

Whilst equity crowdfunding is more of a medium to long term investment, P2P is usually more short term, typically comprising periods of just 6 to 12 months.

This form of crowdfunding is for borrowers who are either not eligible, or for whom bank finance is not suitable . They’re prepared to pay a high interest rate for a short period. These borrowers tend to be property developers who are looking to refurbish and ‘flip’ a property, or to use the loan for other business purposes.

Just to elaborate on that for a second: ‘flipping’ property means to raise profit from either buying low and selling high (which works best in a rapidly rising market). It also applies to developers fixing up a rundown property before reselling it for a profit, which is sometimes known as ‘fix and flip’.

These borrowers do pay a premium for these short term ‘bridging loans’, which is great news for lenders. Lenders can usually expect excellent rates of return. With The House Crowd, for example, the typical return is around 9 -12% per annum.

In the same way that a bank would secure a mortgage loan, with P2P your money is secured against the borrower’s property through the registration of a legal charge.

P2P lenders get priority over equity shareholders when it comes to payouts when the property is sold. This, of course, makes for a more secure investment. That is, provided you only invest in properties with a sensible Loan to Value, just in case the borrower defaults and the property has to be sold.

The House Crowd only invests in properties where monies loaned are less than 75% of the property’s RICS valuation. This allows for a decent cushion to fall back on if the property needs to be sold quickly at a discount in order to repay lenders.

The thing with P2P lending is that you don’t receive equity in the property. This means you won’t benefit from capital growth, as you would with equity crowdfunding. However, you will have that plus side of having more predictable returns, as well as knowing how long your money is likely to be tied up.

Bridging finance has been on the scene for several decades, but the emergence of crowdfunding companies democratises the industry. Now, small investors as well as HNWs can engage with this lucrative market, making loans as small as just a few hundred pounds.

Another bonus: soon P2P lending will be available under the Intelligent ISA wrapper, which will make your returns tax-free.

Unlike equity crowdfunding, P2P lending is not Sharia compliant, as interest is paid to investors.

Written by Frazer Fearnhead, The House Crowd

Written by Frazer Fearnhead, The House Crowd

Frazer started his career as a lawyer in the music industry. He has been investing in property since 1994 and working with other investors since 2003, helping them invest in over £60,000,000 worth of investment property along the way. He is the founding director of The House Crowd – www.thehousecrowd.com – the world’s first property crowdfunding platform.