House Price Index

Sales surge pushes new-to-market prices to record high

- Average new seller asking prices hit record high of £312,625, pushing annual price growth to 3.5%

- Record prices fuelled by strong buyer demand and lack of supply compared to the same period a year ago:

- Number of sales agreed up by 17.8%, to the highest at this time of year since 2016

- Properties selling an average of 6% faster nationally, and 18% more quickly in London

- Disparity between supply and demand as new seller numbers rise by just 1.2%

- Rightmove recorded five busiest days ever in February

- Hard to predict how post-election boost will be affected by unknown impact of coronavirus

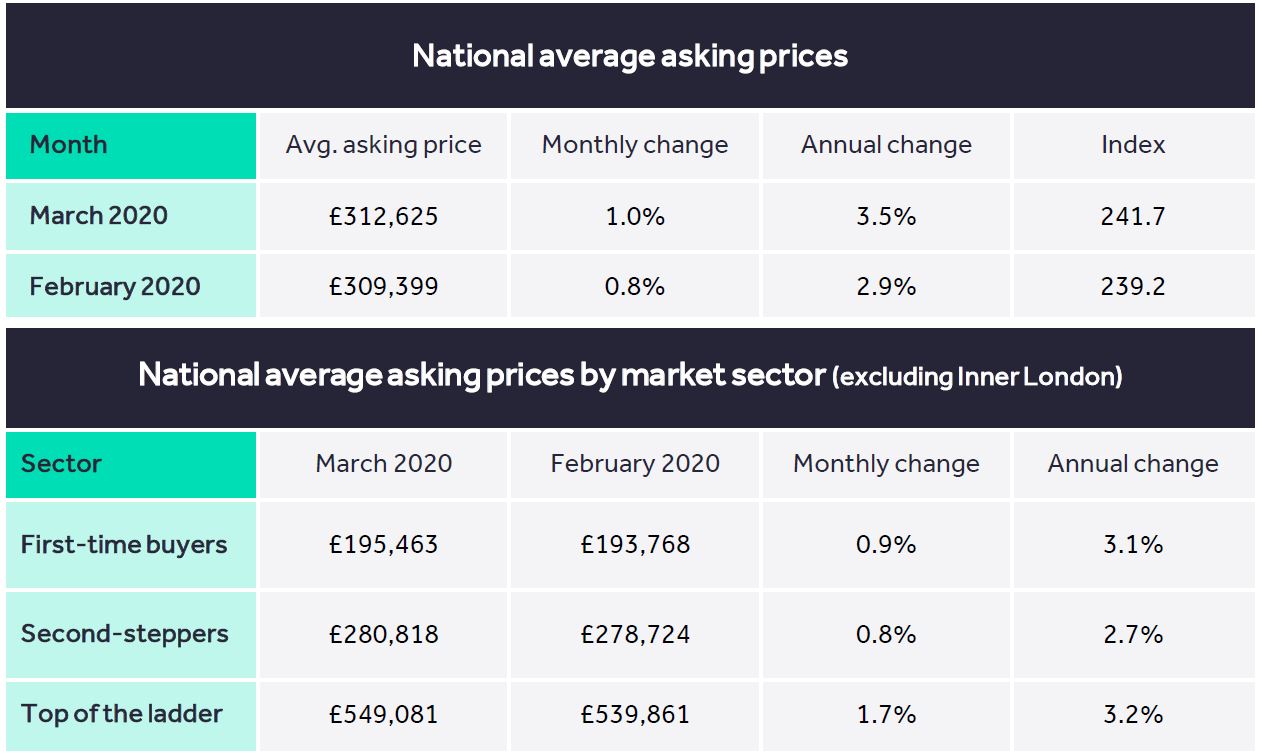

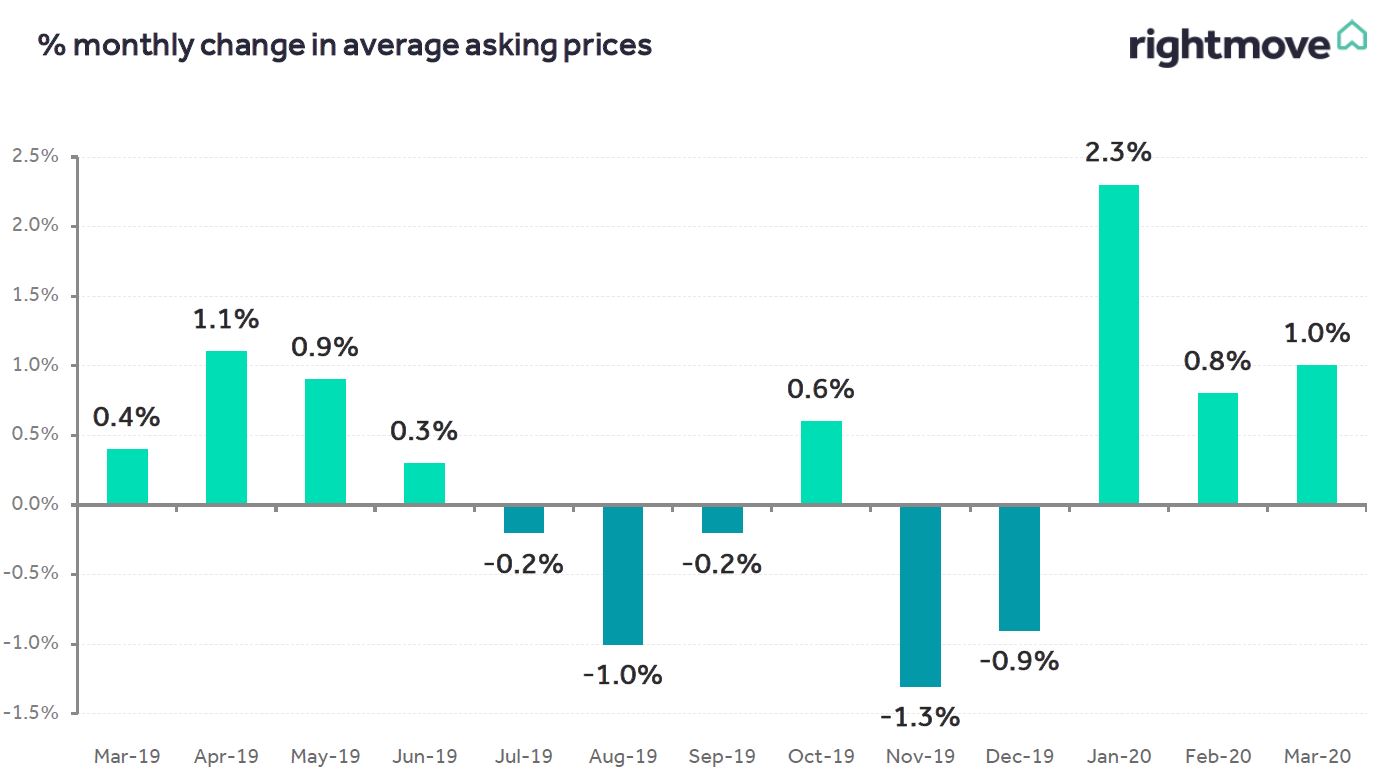

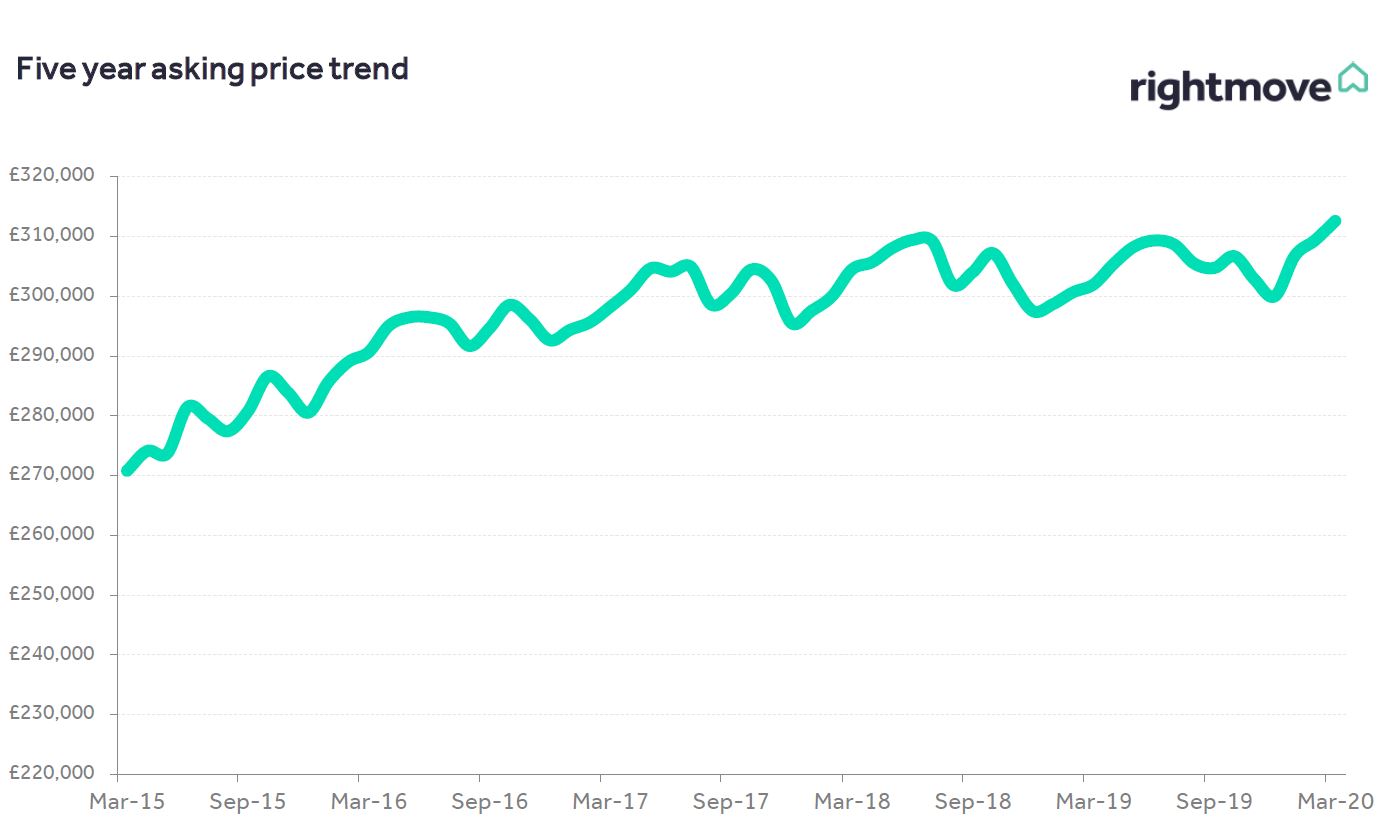

The average asking price of property coming to market has hit a new all-time high, beating the previous record set in June 2018 by some £3,186. This month’s 1.0% (+£3,226) monthly rise has pushed the average up to £312,625, up by 3.5% compared to a year ago. This is the highest annual rate of price growth since December 2016. The key metrics so far all point to a much more active market than last year, fuelling upwards price pressure.

Miles Shipside, Rightmove director and housing market analyst comments: “The average asking prices of over 110,000 properties that have come to market this month are at a record high as we enter the traditionally busy spring moving season. As a result, we are measuring the highest annual rate of increase since December 2016. Many more properties are being bought, and bought more quickly than at this time last year. This is further fuelling the existing shortage of property available for sale, driving up prices to a new record high.”

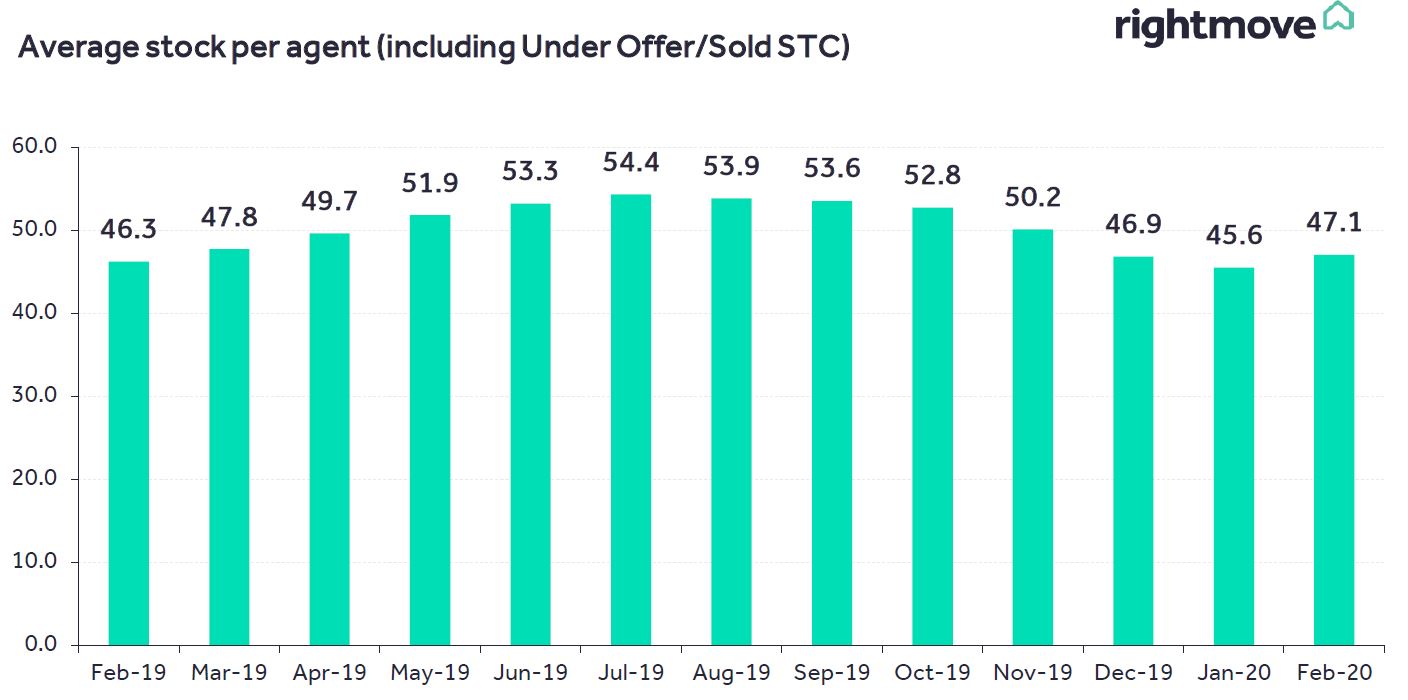

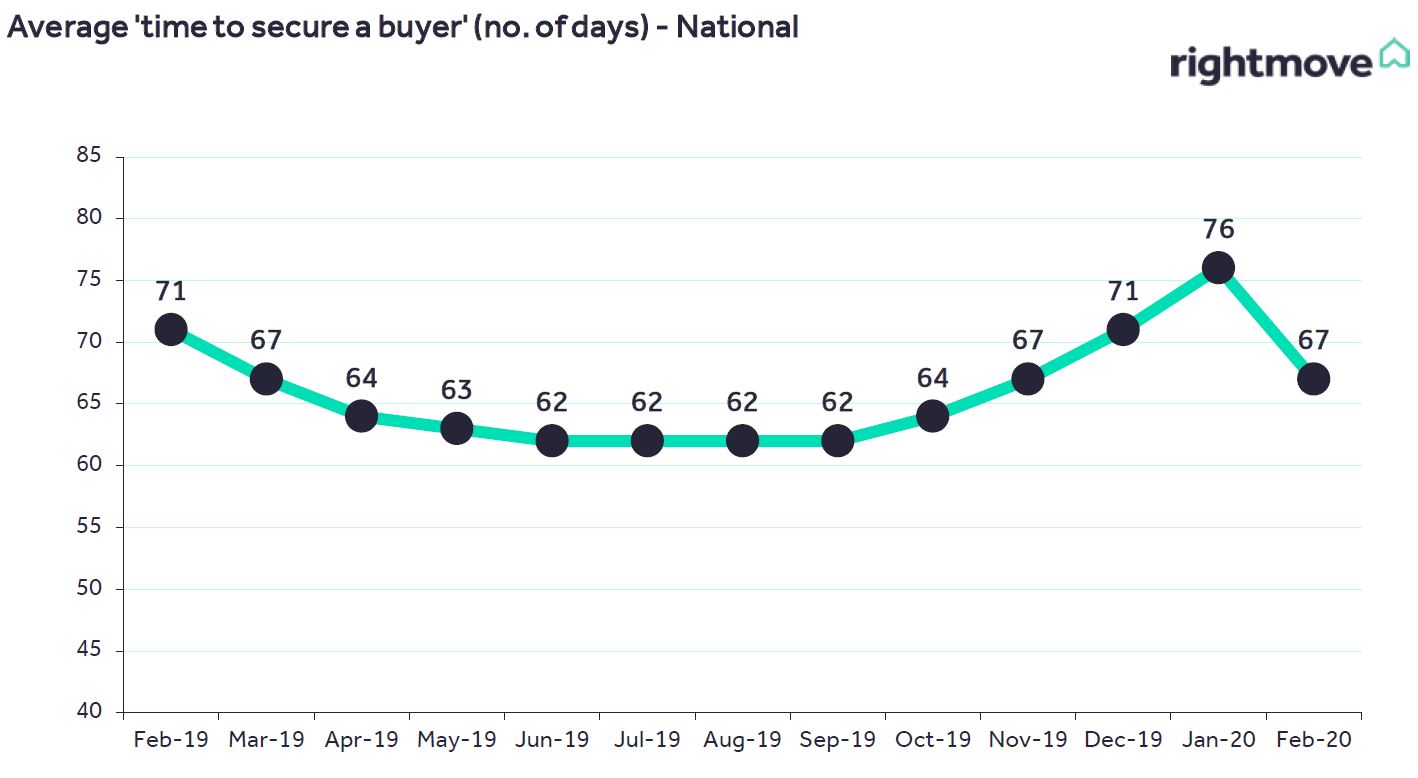

Properties are selling an average of 6% faster nationally compared to this time last year, with the average time to sell now 67.0 days, down from 71.4 days a year ago. The improvement in the time taken to find a buyer is most marked in London, which is 18% faster (15 days quicker) than 12 months ago. Nationally the number of sales agreed is up by 17.8% year-on-year, which is at the highest level for this time of year since 2016. This strong demand has not been matched by new supply with new seller numbers rising by just 1.2%.

Shipside adds: “New supply to the market has failed to keep anything close to the pace of demand. Purchasers in a position to buy have been snapping up what’s currently on the market, rather than waiting for the usual post-Easter flurry of fresh supply. There are marginally more owners putting their properties on the market compared to this time last year, but it is usual for sellers to want to wait for another month or two until there are more leaves on the trees to soften the starkness of their photographs and harden up their pricing prospects.”

It is hard to predict how this post-election boost in market activity will be affected by the unknown impact of the Covid-19 coronavirus. Last week’s Budget mainly focused on this issue rather than on housing and major stamp duty reforms. Whilst any savings in stamp duty would have been welcomed by purchasers, Rightmove’s latest statistics indicate that the market fundamentals remain broadly sound. The new 2% stamp duty surcharge for non-UK residents may eventually temper the current recovery in some sectors of the London market from April 2021, though it will also provide a negotiating advantage to UK buyers. The Bank of England’s unexpected interest rate cut to 0.25% may also help to support the housing market if it feeds through into lower mortgage interest rates.

Shipside notes: “The market has been waiting for several years for a window of certainty, and 2020 seemed set to be the year when many would look to make a move and satisfy their pent-up housing needs. However, the current fast pace of the housing market could now be temporarily affected by the spread of the Covid-19 coronavirus. We expect that housing market statistics, like other economic indicators, could be prone to volatility over the spring and summer. However the market fundamentals are still very sound, hence the current surge in activity, which has included Rightmove’s five busiest days ever. There have been no signs so far of a drop in buyer activity or interest in the housing market.”

Agents’ views

Nick Leeming, chairman of Jackson-Stops, said: “In line with the rest of the industry many of our branches registered a ‘Boris Bounce’, with our network reporting a 10% increase in the number of new applicants registering on the year to January. This renewed confidence has encouraged sellers to push for slightly higher guide prices than they would have six months ago – in turn marginally increasing local asking prices. While nationally stock remains limited, our branches saw a 26% uplift in new instructions in January compared to the same month a year ago, and we expect this to continue as we approach the busy spring market. Those looking to move soon should start speaking to their local agent now with a view to launching while competition remains fairly low and borrowing costs are back down to the lowest level in history following the Bank of England’s cut to interest rates. As an industry, we are yet to see the impact of Covid-19 on the market, however if fewer people opt to holiday abroad over summer, we could perhaps see an increase in activity in this traditionally slower period.”

Glynis Frew, CEO of Hunters, said: “The election dust has settled but buyers and sellers haven’t taken their foot off the gas, with sales picking up both in terms of speed and volume. It’s a nationwide trend but is especially clear in the capital, where the new-found confidence has understandably been felt most profoundly. There’s still a bit of work to be done to address the supply and demand imbalance.”

Sales surge pushes price growth to highest annual rate since 2016

- Price of property coming to market now up by 5.1% year on year, the highest annual rate of growth since May 2016

- Jump in prices fuelled by strong buyer demand and lack of supply compared to same period a year ago:

o Number of sales agreed surges by 34.4%, to the highest at this time of year since 2016

o Quicker time to sell by an average of 18% (fifteen days less)

o Disparity between supply and demand as new seller numbers rise by just 7.9%

o The Budget’s 2% stamp duty surcharge on non UK resident buyers may eventually temper the nascent recover

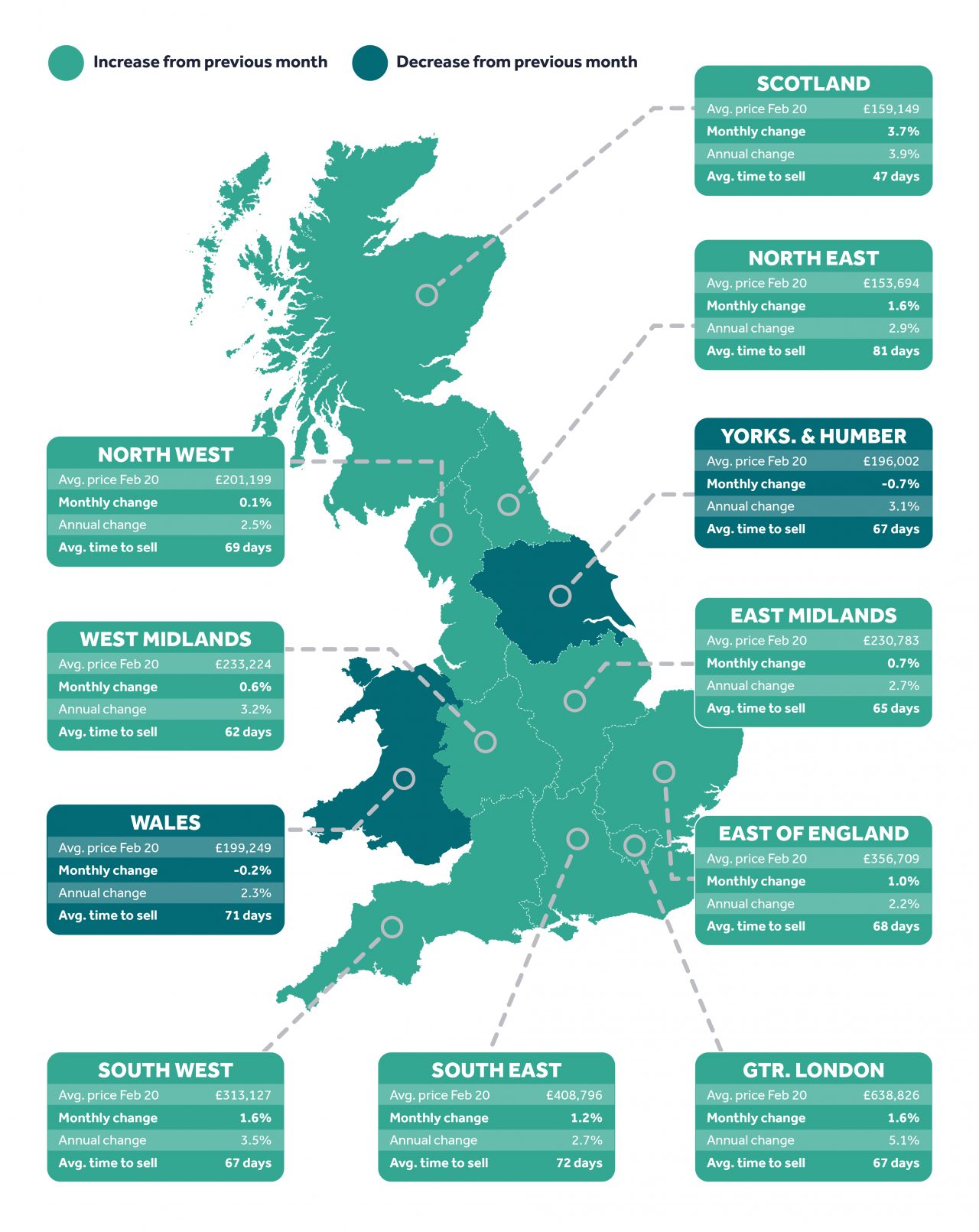

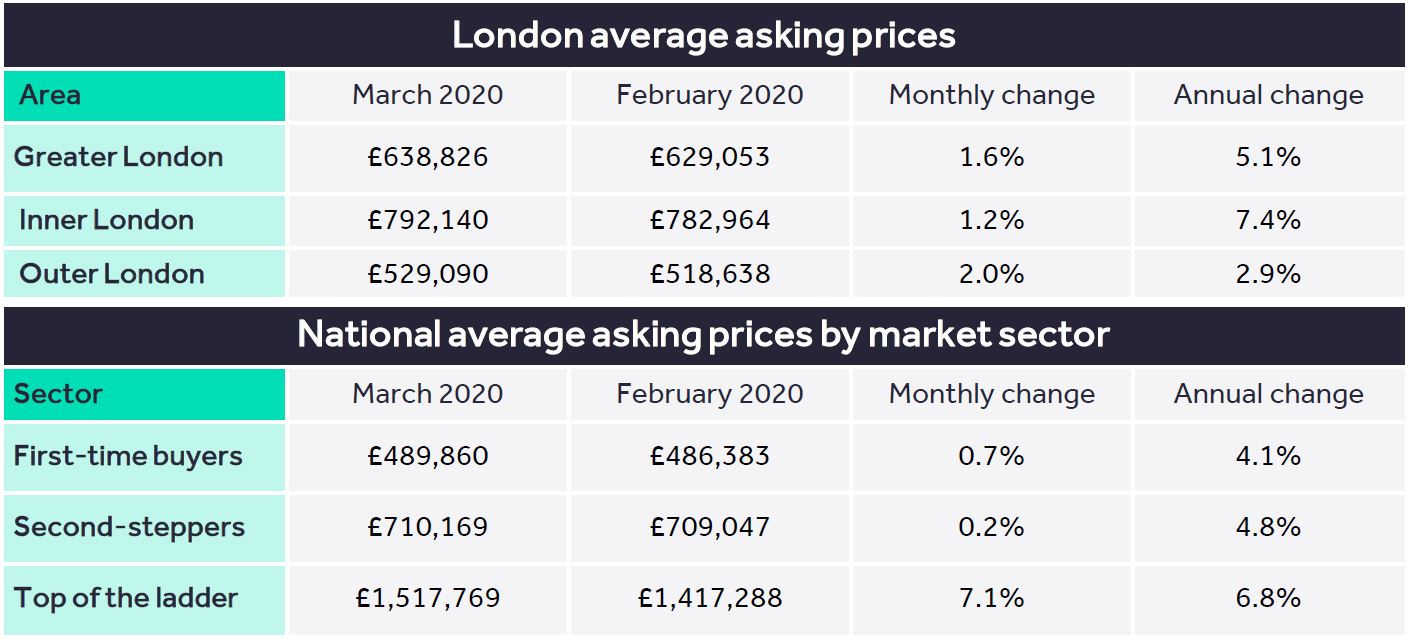

The price of property coming to market in Greater London rises by 1.6% (+£9,773) this month, the largest rise at this time of year since 2014. This jump means that prospective buyers are now facing prices an average of 5.1% higher than a year ago. This is the highest annual rate of price growth since May 2016. The key metrics all point to a much more active market than last year, especially in Inner London, fuelling upwards price pressure.

Miles Shipside, Rightmove director and housing market analyst comments: “Compared to this time a year ago, average asking prices are over 5% higher as we enter the traditionally busy spring moving season. As the turnaround in the capital gathers pace, prospective buyers are now having to contend with prices increasing at the fastest annual rate since M ay 2016. Many more properties are being bought, and bought more quickly than at this time last year. This is further fuelling the existing shortage of property available for sale, driving up prices in the areas that are leading London’s recovery.”

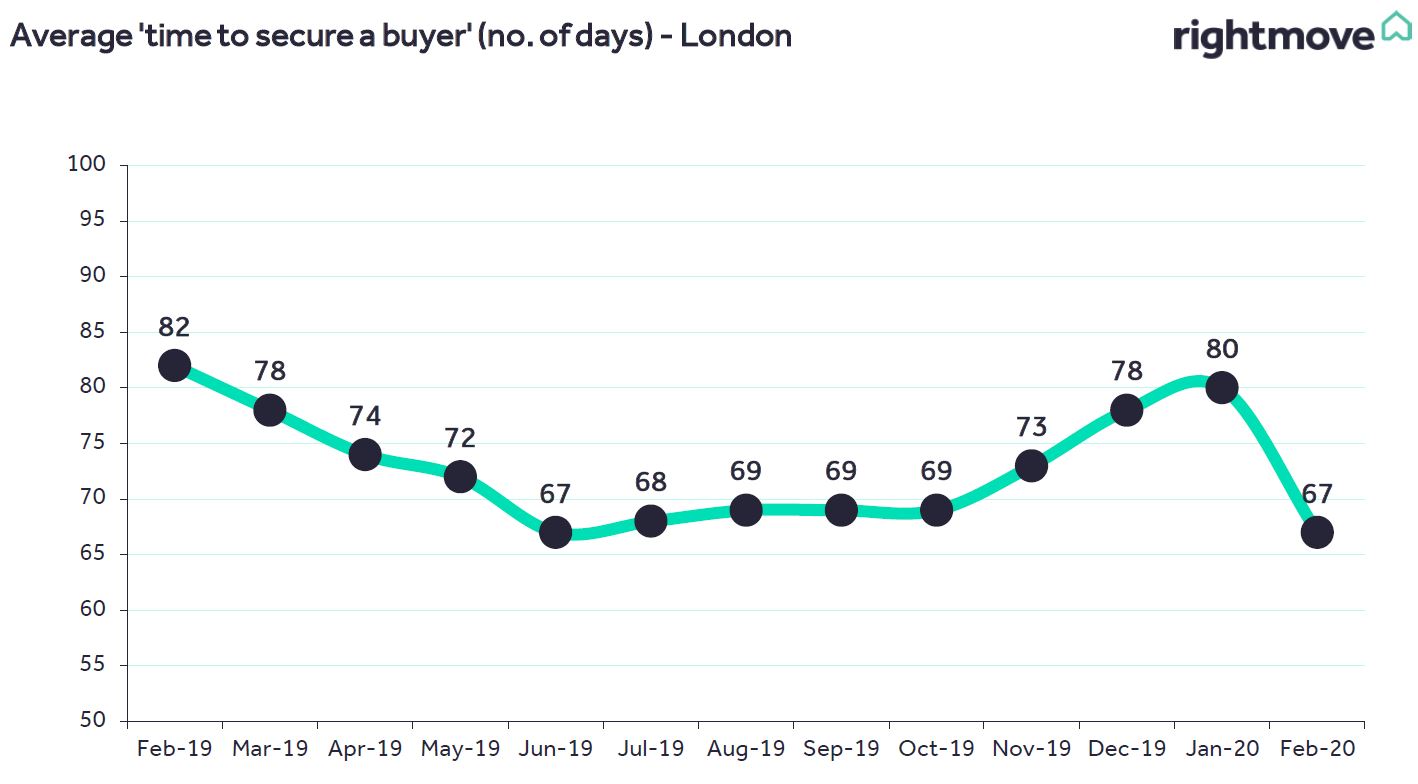

Properties are selling an average of 18% faster (fifteen days less) than this time last year, with the average time to sell now 67.2 days, down from 81.9 days a year ago. The number of sales agreed has surged by 34.4% year on year, and is at the highest level seen at this time of year since 2016. This strong demand has not been matched by new supply, with new seller numbers rising by just 7.9%.

Shipside adds: “New supply to the market has failed to keep anything close to the pace of increased demand in this recovery. Purchasers in a position to buy have been snapping up what’s currently on the market, rather than waiting for the usual post Easter flurry of fresh supply. There are more owners putting their properties on the market compared to this time last year, but it is usual for sellers to want to wait for another month or two until there are more leaves on the trees to soften the starkness of their photographs and harden up their pricing prospects.”

It is hard to predict how this post election boost in market activity will be affected by the unknown impact of the Covid 19 coronavirus. Last week’s Budget mainly focused on this issue rather than on housing and major stamp duty reforms. Whilst any savings in stamp duty would have been welcomed by purchasers, Rightmove’s latest statistics indicate that the market fundamentals remain broadly sound. The new 2% stamp duty surcharge for non UK residents may eventually temper the current recovery in some sectors of the London market from April 2021, though it will also provide a negotiating advantage to UK buyers. The Bank of England’s unexpected interest rate cut to 0.25% may also help to support the housing market if it feeds through into lower mortgage interest rates.

Shipside notes: “The market has been waiting for several years for a London recovery. With a window of post election political certainty, 2020 seemed set to be the year when many would look to make a move and satisfy their pent up housing needs . However, the current fast pace of the housing market could now be affected by the spread of the Covid 19 coronavirus. We expect that housing market statistics, like other economic indicators, could be prone to volatility over the spring and summer. However the market fundamentals are still very sound, hence the current surge in activity, which has included Rightmove’s five busiest days ever. There have so far been no signs of a drop in buyer activity or interest in the housing market.”

Agents’ views

Louis Harding, Head of London Residential Strutt & Parker, said: “What we’re seeing in the London market at present follows what the numbers are saying. Our applicant numbers and new registrations are up by close to 40% on last year, and although our stock levels have increased from January, year on year we are still 30% down on combined property. I don’t think we should be overly concerned with the 2% Stamp Duty surcharge on non UK resident buyers, coming into effect in April next year. In the short term, it would seem sensible for a foreign purchaser with an ambition to buy in London for the increased duty charge to inform part of their decision making process. The 2% surcharge will be quickly absorbed by the market with buyers factoring this in when placing a bid on a property. Most non UK buyers who are buying in London are doing so for medium to long term reasons; as such it’s an additional cost that will be accepted and understood. The additional 2% will put London in line with other global cities such as New York. We are not unique and very much part of a global community. It’s a small world these days, and the increase is unlikely to have a lasting impact.”

Tom Bill, Head of London Residential Research at Knight Frank, added: “There has been a clear response in the London property market following December’s decisive general election result. In the second week of January this year, Knight Frank registered the highest number of new prospective buyers in London for 15 years. However, it should be noted that 2019 was the strongest year since 2014 for prime London markets, having already been in recovery mode. This uptick is the result of price corrections, ultra low interest rates and a weak pound. Despite this upwards momentum, the current volatility on global financial markets and government’s proposed stamp duty changes demonstrate the markets still faces headwinds.”

Nick Leeming , chairman of Jackson Stops, said: “In line with the rest of the industry many of our branches registered a ‘Boris Bounce’, with our network reporting a 10% increase in the number of new applicants registering on the year to January. This renewed confidence has encouraged sellers to push for slightly higher guide prices than they would have six months ago in turn marginally increasing local asking prices. While nationally stock remains limited, our branches saw a 26% uplift in new instructions in January compared to the same month a year ago, and we expect this to continue as we approach the busy spring market. Those looking to move soon should start speaking to their local agent now with a view to launching while competition remains fairly low and borrowing costs are back down to the lowest level in history following the Bank of England’s cut to interest rates. As an industry, we are yet to see the impact of Covid 19 on the market, however if fewer people opt to holiday abroad over summer, we could perhaps see an increase in activity in this traditionally slower period.”

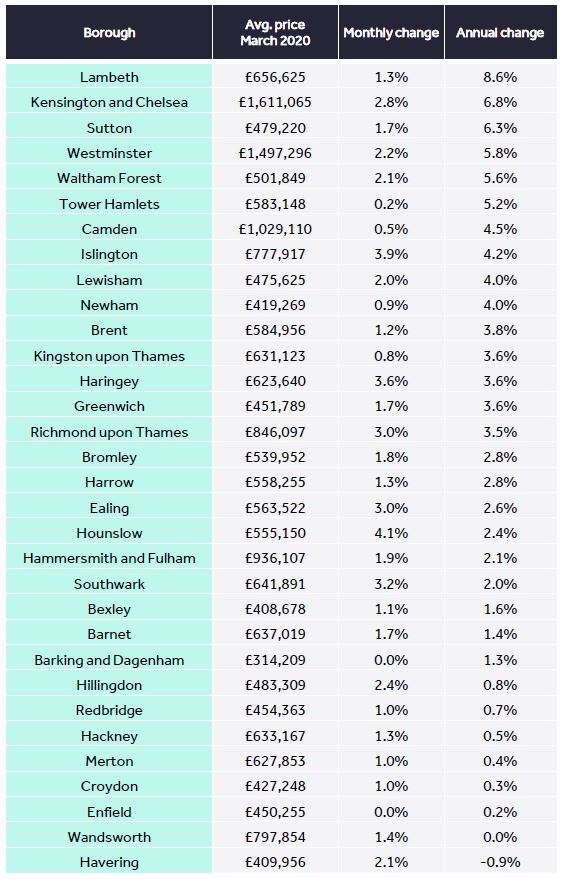

*Borough data is based on a three month rolling average and can be used as an indicator of overall price trends in each borough over time. It is not directly comparable with the overall London monthly figures.

The House Price Index is the largest, most up-to-date monthly sample of residential property asking prices. The index monitors changes in house prices both annually and monthly, providing a comprehensive view on the current state of the property market in England, Scotland and Wales.

Based on circa 95% of newly marketed property, the Rightmove House Price Index is the leading indicator of residential property prices in England, Scotland and Wales.

Contact our press team

Email: press@rightmove.co.uk

Financial PR team

Sodali: Rob Greening / Elly Williamson

Tel: 0207 250 1446

Email: rightmove@sodali.com